Turning operations into a growth engine: New economics for asset servicers

Most asset servicers view their operations as cost centres requiring careful management.1 The focus becomes efficiency, error reduction, and cost control. Whilst these matter, this framing misses a fundamental opportunity. Operations can become sources of competitive advantage and revenue growth, rather than constraints to be managed.

The distinction between servicers achieving this transformation and those remaining trapped in traditional cost-centre thinking is creating divergent market positions. Understanding what separates them reveals possibilities most servicers haven’t fully considered.

The strategic value of operational architecture

The conversation about operational capability typically centres on keeping pace with current demands. Can you handle your existing client base? Can you process transactions accurately? Can you meet reporting deadlines?

A different set of questions reveals strategic potential. Can your operations enable services you don’t currently offer?2 Can they support client segments you’ve considered but dismissed as too complex? Can they create experiences that generate loyalty beyond contractual switching costs? Can they fund innovation through efficiency gains?

When operations answer these questions positively, they stop being cost centres and become growth engines. The shift isn’t semantic. It changes what you can sell, how you compete, and which markets you can enter profitably.

Recognising true operating leverage

Operating leverage in asset servicing manifests differently than in many industries. It’s about how marginal complexity affects marginal cost.

Consider client onboarding. Some servicers experience this as a multi-month process requiring significant resource allocation regardless of client size. Others configure new clients in weeks with minimal disruption. The difference isn’t effort or expertise. It’s whether your operational architecture accommodates variation through configuration or requires customisation.3

Service launches tell a similar story. Launching a new reporting product might require months of development, testing, and deployment in one environment. In another, the same capability emerges through platform configuration in weeks. One servicer enters a new market opportunity whilst competitors are still scoping requirements.

Revenue per employee becomes revealing not as a pure efficiency metric but as an indicator of operating leverage. When this metric improves whilst service quality increases, it signals operations structured to handle complexity without proportional resource increases.

The servicers achieving this leverage aren’t working harder. They’ve built operational architectures where complexity gets absorbed by the system rather than multiplying manual work.

Commercial implications of operational capability

Operational architecture shapes commercial possibilities in ways that become visible only when you examine what different servicers can pursue profitably.

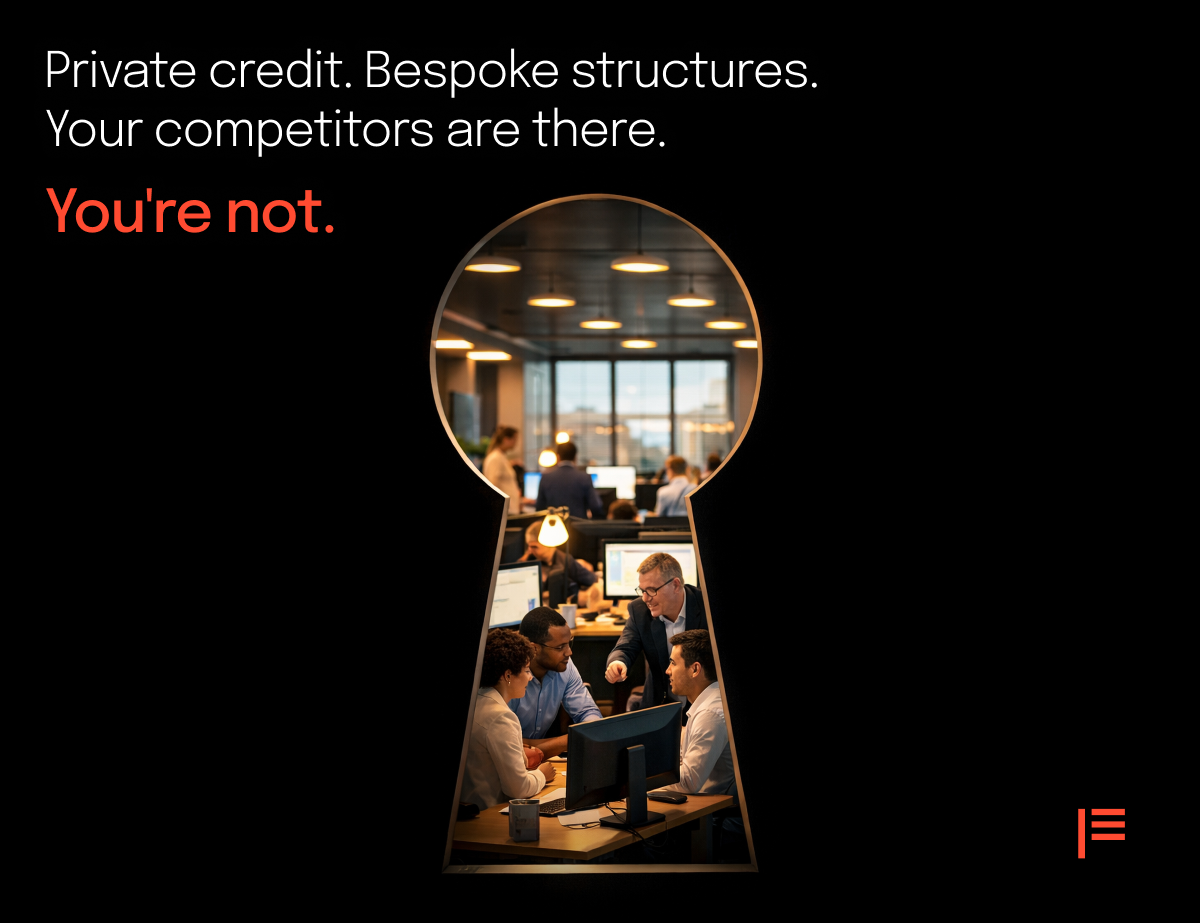

Addressable market expansion. Certain market segments appear attractive commercially but operationally prohibitive for many servicers. Complex private credit structures, bespoke co-investment arrangements, or highly customised reporting requirements fall into this category.4 For servicers whose operations handle complexity gracefully, these segments become growth opportunities rather than operational nightmares.

Competitive positioning. Procurement processes increasingly probe operational capability directly.5 Implementation timelines, portal demonstrations, and reporting flexibility aren’t supplementary considerations. They’re primary evaluation criteria. When your operations enable you to commit to speeds or service levels competitors can’t match, you’ve created competitive differentiation through operational capability.

Pricing flexibility. When operational costs scale linearly with complexity, pricing must reflect cost recovery with limited margin flexibility.6 When operational architecture reduces marginal costs substantially, pricing can emphasise value delivered. This enables aggressive pricing where needed whilst protecting margins on complex mandates.

Client retention through experience. Contractual switching costs provide some retention protection, but client experience creates genuine loyalty. When your operational capability enables superior digital experiences, flexible reporting, and rapid response to requests, clients stay because they prefer your service, not because switching feels onerous.

The investment logic

Achieving operational leverage requires investment in different infrastructure than most servicers currently maintain. Traditional operational investment follows predictable patterns: maintain current capability as systems age,7 address specific bottlenecks, meet regulatory requirements. These investments deliver necessary maintenance but rarely transform what you can accomplish.8

Investment in operational architecture follows different logic. You’re building capability to handle future complexity without future resource increases, launch services rapidly, configure client-specific requirements without custom development, scale revenue without scaling headcount proportionally, and enter new markets your current operations can’t support profitably.

The business case isn’t built primarily on cost reduction. It’s built on revenue enablement9: markets you can serve, mandates you can win, services you can launch, margins you can protect.

Characteristics of growth-engine operations

Rather than prescribing specific solutions, it’s more useful to describe characteristics that distinguish operations functioning as growth engines.

They demonstrate configuration capability rather than requiring custom development for client-specific requirements. They exhibit predictable, short implementation timelines that become competitive advantages. They generate consistent, positive client feedback about technology capability. They enable teams to focus on client service and innovation rather than system maintenance. They support multiple asset classes and complex structures without operational strain.

Most tellingly, they create compounding advantages over time. Each improvement builds on previous capabilities. The gap between what you can deliver and what competitors offer widens progressively.

The strategic choice

Every asset servicer faces a fundamental choice about operational architecture. You can continue managing current operations with incremental improvements, make selective investments in specific areas, or commit to comprehensive operational transformation.

None of these paths is universally correct. The right choice depends on your market position, competitive threats, growth ambitions, and strategic vision. What’s increasingly clear is that operational capability increasingly determines which servicers will lead their markets.10

The servicers that will dominate asset servicing won’t necessarily be the largest today. They’ll be the ones who recognised that operational architecture creates strategic options, and who invested accordingly whilst others focused solely on managing costs.

The question isn’t whether your operations could become a growth engine. It’s whether you’ll make the strategic choices required to transform them into one.

This article is part of our asset servicing insight series

Citations

1 81% cite fee pressures from asset managers as a significant business challenge. Cost savings (79%) and ROI (71%) are the primary AI/GenAI performance metrics. Deloitte 2025 AS Survey, p.29–30, p.39

2 75% of servicers are extending product offerings to include front-office activities (up from 33% in 2023). 93% plan to develop digital assets capabilities within five years. Deloitte 2025 AS Survey, p.33–34, p.35

3 62% cite integration challenges and process fragmentation as major drawbacks of point solutions; 47% cite lack of customisation. EY Lux Benchmarking 2025, p.14

4 Private debt is the #1 alternatives growth opportunity. 83% investing in mid/back-office automation and operational efficiency for private markets. Deloitte 2025 AS Survey, p.47–48

5 Flexibility, interoperability, and vendor alliances are now key to winning F2B mandates. Asset managers leverage competitive RFPs for bespoke builds and vendor integrations. Deloitte 2025 AS Survey, p.33–34

6 Pricing models projected to shift from AUM-based to value-based as servicers become digital-first entities offering products and services. EY Lux Benchmarking 2025, p.20

7 Core systems modernisation accounts for 20% of budgets today but is expected to fall to 13% by 2030, as firms shift spend toward digitalisation and innovation (rising from 27% to 38%). Deloitte 2025 AS Survey, p.11–12

8 92% report legacy systems constrain innovation. Legacy technology is the #1 challenge for delivering F2B platforms (also 92%). Deloitte 2025 AS Survey, p.13–14, p.35–36

9 Top digitalization driver has shifted from cost reduction (2022) to operational improvements and customer experience (2024–2025). 90% now prioritise customer experience when investing. EY Lux Benchmarking 2025, p.8, p.11

10 82% of firms prioritise legacy modernisation; 55% investing in real-time analytics and next-gen portals. 28% self-identify as digital front-runners — unchanged since 2023. Deloitte 2025 AS Survey, p.9–12