The asset management and asset servicing transformation playbook: key takeaways from our Luxembourg executive evening

On 21 May, FINBOURNE hosted senior leaders from across the Luxembourg asset servicing and asset management community for an afternoon on what real transformation looks like, and where firms consistently underestimate the challenge.

The conversation moved from industry benchmarks to boardroom decisions to a live demonstration of FINBOURNE’s agentic AI in production. Three threads ran through the whole afternoon.

Three things we kept coming back to

Foundations decide outcomes. AI on top of fragmented data, spreadsheets and weakly governed processes produces incremental gains at best and new operational risk at worst. The firms making real progress have done the unglamorous work on data foundations first.

Build versus buy is being re-litigated. Decisions made five or ten years ago look very different today. The catalogue of failed attempts to build EDM and book-of-record infrastructure internally is long, and the work is genuinely hard. The bar for building should be IP that genuinely differentiates the business, not attachment to the idea of building.

Trust is the rate limiter on AI adoption. The technology works. What is missing in most organisations is the governance, traceability and auditability that lets a board, a regulator and a head of operations sign off on letting agents operate inside critical workflows. Without that, adoption stalls regardless of how impressive the demos look.

Where digitalisation in asset servicing actually stands

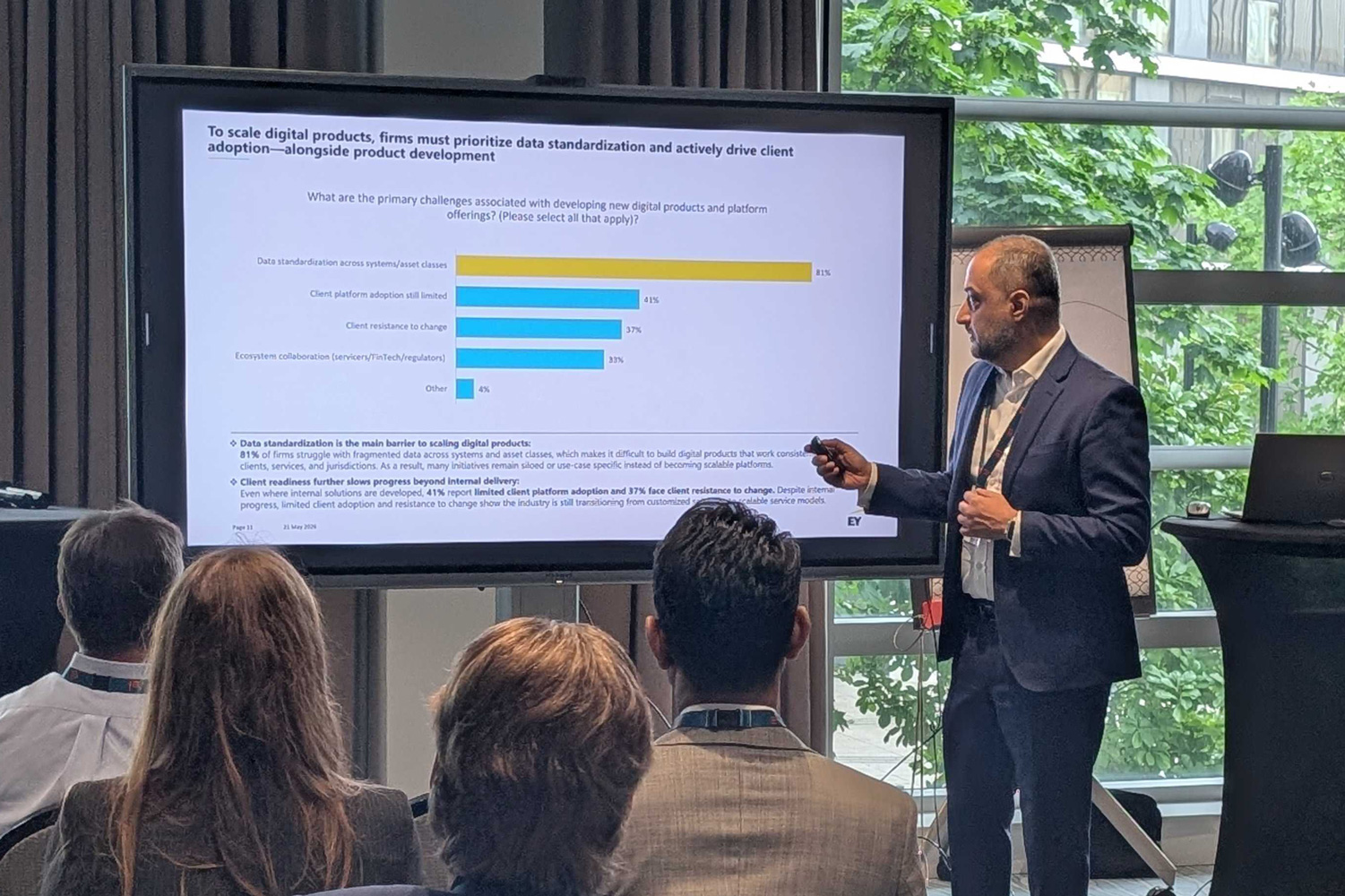

Ajay Bali, Partner and Technology Consulting Leader at EY Luxembourg, opened by sharing findings from EY’s 2026 Asset Servicing digitalisation survey. The data comes from 42 Luxembourg asset servicers, with over 40 per cent responding at group level, benchmarked across strategy and organisation, customer centricity and operations, and technology and innovation. A few findings stood out:

Digital strategy is now mostly top-down. 64 per cent of firms report a group-aligned digital strategy. 25 per cent still rely on function-led, bottom-up initiatives, and more than 10 per cent report no defined digital strategy at all.

Investment is rising but uneven. 67 per cent of firms now invest more than 5 per cent of top-line revenue in digital initiatives, with 30 per cent above 10 per cent. Yet only 19 per cent expect digital products to generate more than 20 per cent of revenues over the next two to five years — investment is going in, but commercial ambition for digital remains modest.

Digital is anticipated in the RFP, but rarely decisive on its own. 63 per cent see digital capabilities as a key differentiator, but only 6 per cent as the primary one. The real shift is in what is being asked: five years ago, asset managers asked whether a provider had a fund accounting platform; two years ago, a data platform; today, they scrutinise the underlying tech stack and run due diligence on it as part of the RFP.

Confidence in AI adoption is broad but shallow. 65 per cent of firms are somewhat confident in adapting to the pace of AI change, but only 26 per cent are extremely confident. EY reads this as a reflection of hybrid architectures, partially mature engineering practices and fragmented data foundations.

AI is being deployed first where rules and data flows are well-defined. Highest adoption is in data ingestion and harmonisation (77 per cent), CRM and onboarding (71 per cent), RFP and DDQ automation (71 per cent) and back-office automation (65 per cent). Use cases requiring real-time orchestration lag materially.

Data standardisation is the dominant barrier to scale. 81 per cent of firms cite fragmented data across systems and asset classes as their primary challenge. Client-side readiness compounds it: 41 per cent report limited client platform adoption, and 37 per cent face active client resistance to change.

Ajay drew a sharp line between “bolt-on” and “build-on” AI. Bolting AI onto existing flows produces incremental gains. Built-on AI, where the process is reimagined around what the technology can do, is where transformative change happens. Most firms are still in the bolt-on phase, which explains why digitalisation budgets are rising faster than measurable productivity.

The full survey is available to download here: Luxembourg Asset Servicing Benchmarking Survey Results 2026.

Rewiring asset servicing: the leadership decisions behind it

Brenda Petsche, Business Consultant and Director and Toby Glaysher, Chairman, FINBOURNE then took the conversation into the questions boards and executive committees are wrestling with right now.

On what separates the firms transforming from the ones talking about it. The industry lacks a common definition of transformation. Spending figures get reported against everything from issuing Copilot licences to genuinely rebuilding the operating model. The firms making progress have understood that organising data and establishing a single source of truth is the prerequisite, and that real-time data flow is what unlocks AI’s value in operational risk and oversight.

On build versus buy. Toby was direct about his own history of building proprietary platforms in a previous role. The catalogue of attempts to build EDM and book-of-record infrastructure internally is long, and most failed not because the architecture was wrong but because the work is genuinely hard and the maintenance burden is permanent. Build only if it differentiates the business.

On regulators and headcount. A well-governed AI agent, with permissioned, traceable and auditable outputs, can deliver better risk control than a team of reviewers working from incomplete data. The conversation with regulators is not about removing oversight, it is about evidencing a different and arguably stronger form of it.

On the board’s role. Boards are not, on the whole, technical enough to adjudicate detailed architecture decisions, and asking them to is the wrong frame. What boards need is leadership they trust to execute, supported by the right governance, measurement and standards.

On the pace of change. The risk of non-adoption is now climbing past the risk of adoption for the first time. But accelerating in the wrong direction, without the data foundations in place, will be worse than moving steadily.

FINBOURNE: the financial operating layer for AI in asset servicing

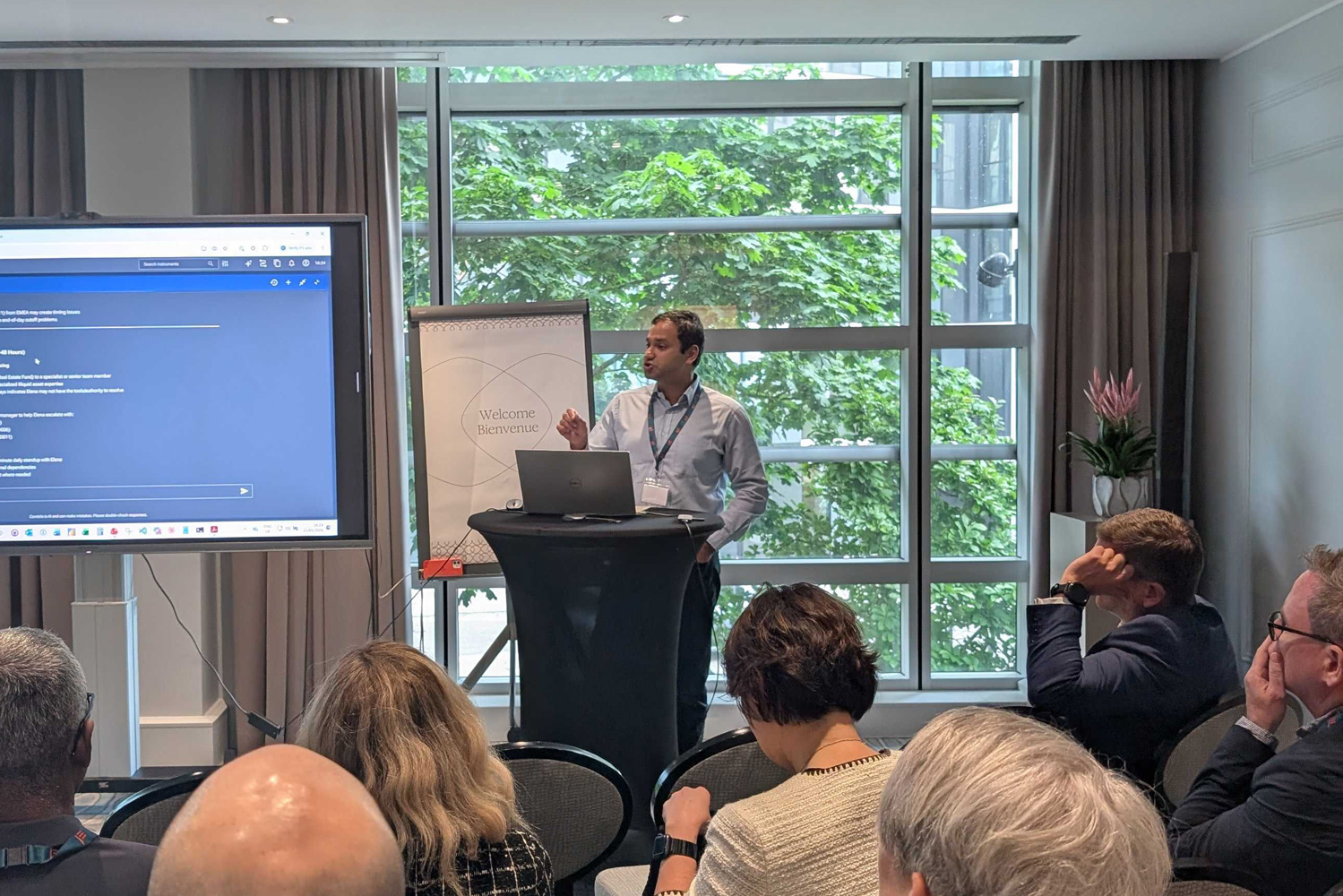

Toby and Rehan Islam, Solutions Architect at FINBOURNE then moved from principles to a live demonstration of AI agents built on FINBOURNE’s data and APIs. Rehan walked through two agents in particular.

The NAV production agent. Framed as a morning briefing for a Head of Fund Accounting, the agent reviewed the previous day’s NAV production, identified which NAVs were late and why, grouped exceptions by root cause, surfaced patterns by region and assignee workload, and produced a prioritised set of recommended actions. The agent is not generating commentary on top of static data, it is calling FINBOURNE’s underlying APIs through an MCP layer that controls and constrains what the LLM is permitted to do.

The fund prospectus agent. Rehan demonstrated the agent processing a multi-share-class prospectus annex and producing several hundred fields of master fund record in around three minutes, with every populated field traceable back to the specific page and paragraph of the source document and tagged with a confidence score. For context, the same work performed by a transition team typically takes around nine and a half weeks.

The architectural point Toby drew out matters most for anyone considering how to deploy this kind of capability. An LLM on its own is a research tool, useful but unsafe in production. An LLM combined with APIs via an MCP server becomes deterministic, permissioned and auditable, with a full audit trail of which agent ran, which tools it called, what data it touched and where every output came from. That combination, not any single component, is what makes the difference between a demo and a deployable system.

Four clients are running these agents in production today on live data, with six more in the pipeline. The target of ten in production by year end is now expected to be reached by mid-year, and the next phase is being shaped by client demand rather than internal hypothesis.

In conversation with Andy Schleck

The afternoon closed with Andy Schleck, winner of the 2010 Tour de France, President of the Tour de Luxembourg, and now Deputy General Manager at one of the leading professional cycling teams. A welcome change of pace, and a generous and engaging conversation with the room before the networking reception.

Our thanks to Ajay Bali from EY Luxembourg for sharing the 2026 survey findings, to Brenda Petsche for leading the conversation, to everyone who joined us in the room, and to Andy Schleck for his time.

If you would like to discuss how FINBOURNE can support your data and AI agenda, from book-of-record consolidation to deploying agents in production, please get in touch.